BLOG

Credit Chat - Get Over Your Fears

When you mention the word "credit" most people shutter! But knowing the facts can help you conquer the fear and get on the path to homeownership!

Join Laura Key, Realtor and Sondra Meadows, Mortgage Loan Expert to get the scoop on credit and how you can fix the most common issues and get on the path to buying a new house or car!

To Reach Laura: laura@laurakey.net

To Reach Sondra: bit.ly/sondrameadows2

Appraised Value: The Ups & Downs Of How Much A House Is Worth

How is the fair market value of a real estate property actually determined?

Determining Fair Market Value is an eternal struggle and major balancing act. That’s because buyers want a house to appraise on the low side—to keep the purchase price down. While sellers want the same house to appraise on the high side—to make the sale price higher. And then you’ve got the owners of the house—who also want the appraisal to be on the low side, in order to keep the property taxes down.

So with all these different agendas and points of view, how is the fair market value of a real estate property actually determined?

Once a year, your county sends all area homeowners official notices that put a dollar value on their property. And property taxes are based on those dollar values. But before those notices get sent out, a long, detailed process usually takes place. First, the land is valued as if it’s vacant—an empty lot, in other words. Then any improvements are described and measured. Improvements consist of the house and any other structures, pools, sheds, garages, and so forth. Next, most counties check the Marshall Valuation Service Cost Guide. It’s a standardized nationwide guide for determining the value of the cost per square foot to build a building that fits the description of the improved property. Next, if the house isn’t brand new, the replacement cost is considered, as well as depreciation; the year the house was constructed and the condition of the property are factors here. Appraisers then must take the critical step of comparing the value of the house with recent selling prices of similar homes in the neighborhood. At this point, the appraisal might stand “as is”—or it might be adjusted upward or downward.

Market Value is a theory, in other words—not an unchanging fact.

In a perfect world, you have to have willing buyer and a willing seller. Neither is under duress. Both are in a position to maximize gain and are trying to do this. But in the real world, things are rarely that simple and equally balanced. Which is why people feel differently about the appraisal value of a house. It really depends how strong their position is as a buyer or seller.

Does the local economy come into it at all? You bet it does.

Ask a successful Realtor about that! He or she will tell you they’ve noticed that the Rio Grande Valley’s fast-growing economy is attracting people from other areas who consider real estate here a bargain. That helps fuel increases in property values.

So—now you know where that Grand Total comes from.

You’re armed with the information you need to make a better house-buying decision. For instance, you can understand how two virtually identical houses that are in two different neighborhoods could be very far apart in price and appraised value. And why your choice of the right house in the right neighborhood could be worth a not-so-small fortune to you right now—and years down the road.

Sellers! You can get a great idea of how much your home is worth! Call me for a FREE Comparative Market Analysis (CMA) Laura Key 310.866.8422

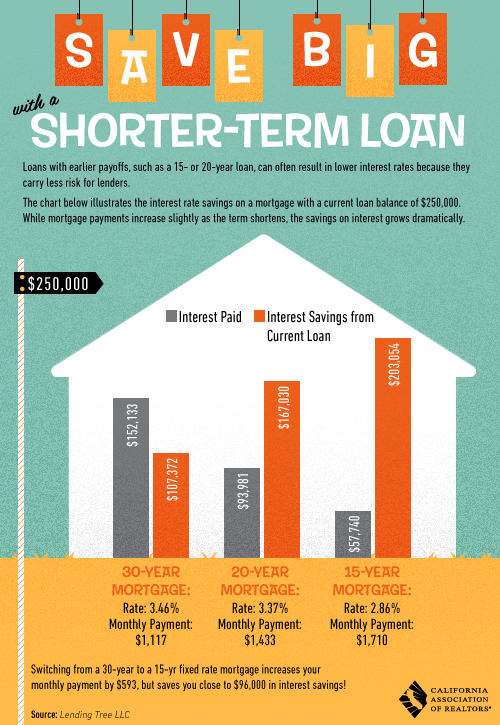

Does Moving Up Make Sense?

Don't get caught up in the madness of the market. Deciding to sell is a personal decision, take everything into account. I am here to assist! Laura Key 310.866.8422

These questions will help you decide whether you’re ready for a home that’s larger or in a more desirable location. If you answer yes to most of the questions, it’s a sign that you may be ready to move.

- Have you built substantial equity in your current home? Look at your annual mortgage statement or call your lender to find out. Usually, you don’t build up much equity in the first few years of your mortgage, as monthly payments are mostly interest, but if you’ve owned your home for five or more years, you may have significant, unrealized gains.

- Has your income or financial situation improved? If you’re making more money, you may be able to afford higher mortgage payments and cover the costs of moving.

- Have you outgrown your neighborhood? The neighborhood you pick for your first home might not be the same neighborhood you want to settle down in for good. For example, you may have realized that you’d like to be closer to your job or live in a better school district.

- Are there reasons why you can’t remodel or add on? Sometimes you can create a bigger home by adding a new room or building up. But if your property isn’t large enough, your municipality doesn’t allow it, or you’re simply not interested in remodeling, then moving to a bigger home may be your best option.

- Are you comfortable moving in the current housing market? If your market is hot, your home may sell quickly and for top dollar, but the home you buy also will be more expensive. If your market is slow, finding a buyer may take longer, but you’ll have more selection and better pricing as you seek your new home.

- Are interest rates attractive? A low rate not only helps you buy a larger home, but also makes it easier to find a buyer.